ACH Debit transaction clearing process

ACH debit transactions are processed in batches, in clearing cycles.

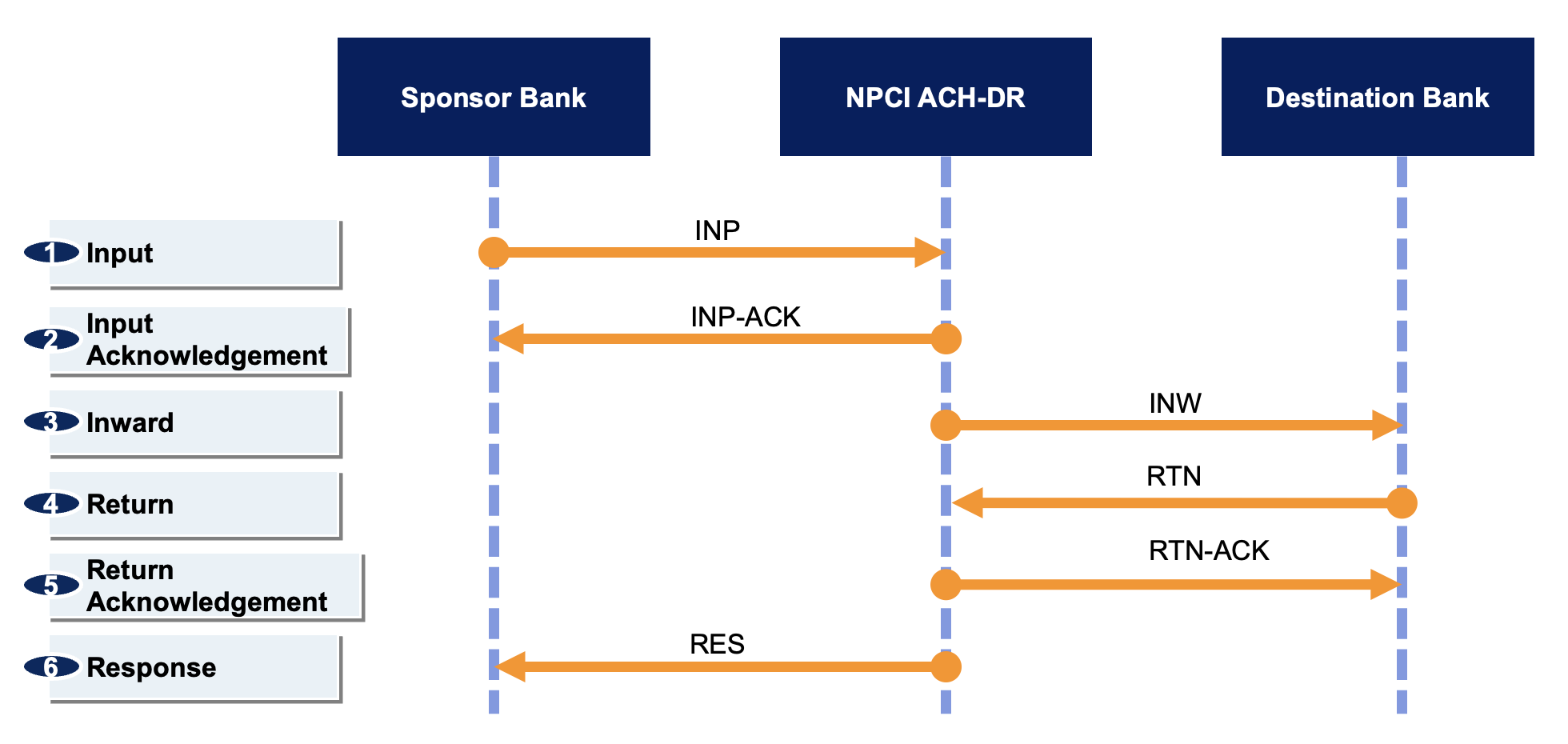

NPCI receives inputs from sponsor bank, sends inwards to destination bank, receives returns from destination bank, and sends responses to sponsor bank. This process is known as clearing, and it is done in batches via file exchange. Clearing happens in cycles which are at fixed times of the day.

Input

Sponsor banks send transaction input batches to NPCI. This is known as INPUT (INP). For a particular charge date, the sponsor bank can send the inputs up to one week in advance, but most tend to do it the day before the charge date, or on the morning of the charge date.

Input Acknowledgement

Upon INPUT submission by the sponsor bank, NPCI immediately validates and gives a receipt. This is known as INPUT ACKNOWLEDGEMENT (INP-ACK). These acknowledgements also mark transaction rejections by NPCI. For example, for any unrecognised UMRN or for any mandate that is not in active status, NPCI will reject the transaction input. Such rejected transaction are not forwarded to destination banks.

Presentation

The INPUT batches that NPCI receives up to a presentation cycle's cutoff time are entered into clearing in that cycle. e.g. if an INPUT is sent at 23:00 on T-1 (the day before the charge date), it enters Cycle 1. e.g. if an INPUT is sent at 07:55 on T (the charge date), it enters Cycle 2.

Presentation cycles:

Cycle 1: 06:00

Cycle 2: 08:00

Cycle 3: 10:00

Cycle 4: 12:00

Final Cycle: 14:00

Inward

NPCI reorganises the sponsor bank's INP batches into dedicated batches for each destination bank. This is known as INWARD (INW). The destination bank receives the INW, and validates and decides how to respond to each transaction request.

For example, if Sponsor Bank A sends INP batch with Transaction 1 and Transaction 2 for Destination Bank B and Transaction 3 for Destination Bank C, then the INW batch for Destination Bank B will contain Transaction 1 and Transaction 2, and the INW batch for Destination Bank C will contain Transaction 3.

Return

The destination bank decides which transactions to return. By default, if they do not return a transaction, it is understood to be accepted.

The destination bank sends RETURN (RTN) batches to NPCI. The RTN batches that NPCI receives up to a return cycle's cutoff time are entered into clearing in that cycle. e.g. if RTN is sent at 08:10 it enters Cycle 1. e.g. if RTN is sent at 18:30, it enters Final Cycle.

NPCI acknowledges RTN with RTN-ACK.

Return cycles:

Cycle 1: 08:00

Cycle 2: 10:00

Cycle 3: 12:00

Cycle 4: 14:00

Cycle 5: 16:00

Cycle 6: 18:00

Final Cycle: 20:00

Response

NPCI receives the RTN batches from destination banks, and reorganises them into dedicated response batches for sponsor banks. This is known as RESPONSE (RES). These RES batches match the INP batches that the sponsor bank originally sent.

The sponsor bank, upon receiving the RES, updates the status of each INP transaction, and informs the service provider or creditor of the status via reports.

Funding

Along with the file exchange process in each clearing cycle, NPCI sends settlement funds to banks.

INPUT: NPCI gives/takes net funding to/from the bank. This is the aggregate sum of all INPUT transactions presented as sponsor bank, minus the aggregate sum of all INWARD transactions for the same bank as destination bank. For example, if Bank A as sponsor bank presents input transactions totalling Rs 100 Cr, and the same bank as destination bank receives inward transactions totalling Rs 60 Cr, NPCI immediately gives that bank funding of Rs 40 Cr.

RETURN: NPCI gives/takes net funding to/from the bank. This is the aggregate sum of all RETURN (denied) transactions sent as destination bank, minus the aggregate sum of all RETURN (denied) transactions notified as sponsor bank. For example, if Bank A as destination bank sends return notices totalling Rs 10 Cr (e.g. bounced due to insufficient balance in the customer's bank account), and the same bank as sponsor bank receives return notices totalling Rs 7 Cr (i.e. it was overpaid that amount in the INPUT cycle), NPCI pays net Rs 3 Cr to that bank.

In this way, at the end of of the day after all clearing cycles, the net funding position of the bank equals the total of all confirmed transactions requested as sponsor bank minus the total of all confirmed transactions payable as destination bank. In the above example, overall Bank A was entitled to Rs 90 Cr as sponsor bank and should pay Rs 57 Cr as destination bank i.e. net it should receive Rs 43 Cr. As per clearing cycles, it received Rs 40 Cr plus Rs 3 Cr i.e. net it received Rs 43 Cr.

As funds requested by the sponsor bank are already collected from the destination bank in the INPUT cycle, if that destination bank bank fails to return a transaction for insufficient balance or any other reason in the RETURN cycle, they stand to lose. Therefore destination banks act promptly to avoid the punitive loss. Rarely they are late in sending returns, and this leads to a difficult situation where they have to manually ask the sponsor bank to send the funds back for specific transactions. This is known as 'late return', and is akin to chargebacks in other payment systems.

The sponsor bank is responsible for giving the collected funds to the creditor. How and when they do it is up to them, and is not related to the ACH Debit clearing system. NPCI encourages sponsor banks to give the funding to the creditor as soon as possible. Ideally the sponsor bank should give the collected funds from each cycle (the sum of all confirmed transactions) to the creditor immediately after the cycle. However, in practice most sponsor banks give a single aggregate funding payout to the creditor at the end of the day, after the Final Cycle. The exception to this is for mutual funds.

Special process for mutual fund activity

There is a special process for mutual fund activity to ensure the end customer gets NAV of the same value date that funds are debited from their bank account. The entire batch processing is separate for mutual fund transactions as these batches are tagged MUT, but they follow the same clearing cycles as for all other transactions. The sponsor bank should ensure to present the MUT batches as early as possible - ideally in Presentation Cycle 1 at 06:00, and certainly no later than Presentation Cycle 3 at 10:00. As the mutual fund batches are tagged as MUT, the destination bank knows that it has to respond to those batches on priority, and certainly no later than Return Cycle 3 at 12:00. In this way, the sponsor bank receives the funds by 12:00 and can give the responses and funding to the creditor (i.e. the mutual fund) asap, thus ensuring that the mutual fund will provide the end customer with the same day NAV.

Notes

NPCI's 2022 changes increased the number of Presentation and Return cycles, meaning creditors get some transaction responses earlier in the day. If the sponsor bank has streamlined their funding regime, they can give the funding to the creditors earlier in the day too.

NPCI has taken this step to make the NACH Debit payment system closer to real time, and is encouraging sponsor banks to give intra-day settlement payouts to creditors.

NPCI NACH Circular 2022-23/001![]() (8 April 2022) explains the reorganisation of ACH sessions. This took full effect on 5 June 2022. However, further adjustments were made by NPCI without publishing any circular e.g. presentation cycles were reduced from eight to five, and the T-1 session for mutual funds and legacy was removed entirely.

(8 April 2022) explains the reorganisation of ACH sessions. This took full effect on 5 June 2022. However, further adjustments were made by NPCI without publishing any circular e.g. presentation cycles were reduced from eight to five, and the T-1 session for mutual funds and legacy was removed entirely.